IRS-qualified art appraisals for charitable donations, meeting Form 8283 Section B requirements over $5,000. AppraiseItNow provides USPAP-compliant fair market value reports for donated artwork, helping donors maximize deductions with confidence.

Best in class appraisers across asset types

.avif)

Joe Kattan

Anne Hay, ISA AM

Ashley Innes, ISA AM

Aron Blue

Artwork Appraisals for Charitable Donation

When you donate artwork to a qualifying organization and claim a federal tax deduction, the IRS requires a qualified appraisal for any single work or group of similar items valued above $5,000. That appraisal must establish fair market value as of the donation date, comply with USPAP, and support the completion of Form 8283 Section B, which requires signatures from both the appraiser and the donee organization. For artwork valued above $20,000, the full appraisal must be attached to your tax return, and high-resolution photographs may be requested by the IRS. Our art appraisal team handles all of this with the documentation depth the IRS expects.

AppraiseItNow delivers artwork appraisals both online and onsite across the United States, making it straightforward to meet IRS timing requirements regardless of where the donation occurs. Whether you need a single painting valued or a multi-piece collection assessed before a museum gift, our charitable giving appraisal services are structured to fit your timeline and filing deadlines. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Artwork We Appraise for Charitable Giving

AppraiseItNow covers a wide range of artwork categories commonly donated to museums, universities, nonprofits, and cultural institutions.

- Oil, acrylic, and watercolor paintings by listed and emerging artists

- Works on paper including drawings, pastels, and prints in limited or open editions

- Photographs, including fine art prints and vintage photographic works

- Sculptures in bronze, stone, ceramic, glass, and mixed media

- Tapestries, textile art, and fiber works with documented artistic provenance

- Posters and original graphic art with collectible or historical significance

- Folk art, outsider art, and self-taught artist works

- Digital art and NFT-backed physical works with verifiable provenance

- Installation components and conceptual art pieces with documented exhibition history

- Works from estate collections where attribution, condition, and market comparables require careful analysis

How Our Artwork Appraisal Process Works for Charitable Donations

Our appraisers hold credentials through recognized professional organizations including ISA, ASA, and AAA, and are qualified under IRS standards to sign Form 8283 as the appraiser of record.

- Appraisals are completed within the IRS-required window: no earlier than 60 days before the donation date and no later than the due date of the tax return on which the deduction is claimed, including extensions.

- Each report documents the artwork's physical description, condition, provenance, exhibition history, and comparable sales data drawn from auction records and dealer markets, giving the IRS the factual basis it needs to support the claimed deduction.

- For works valued above $20,000, the report is formatted to meet the attachment requirements for the tax return, and photographs are included at the resolution the IRS may request.

- Clients receive a complete, signed appraisal report that the donee organization can reference when completing their portion of Form 8283, along with guidance on what to retain for your records in the event of an audit.

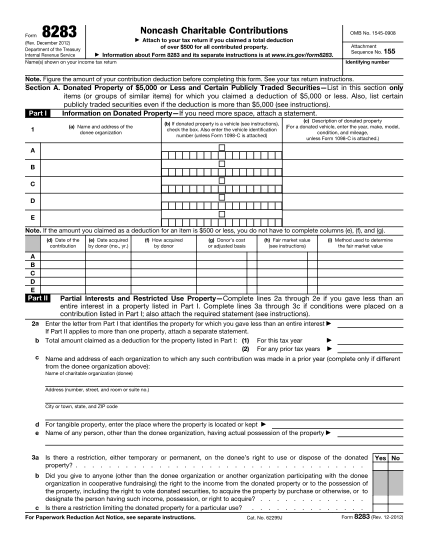

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does an Artwork appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does an artwork appraisal for charitable donation involve?

A charitable donation artwork appraisal is a qualified appraisal report prepared by an independent, credentialed appraiser to determine the fair market value of artwork you intend to donate to a qualified charity for federal income tax deduction purposes. The report includes detailed descriptions, provenance research, condition notes, comparable sales analysis, and photographs, all structured to meet IRS requirements. It supports Form 8283 Section B, which must be signed by both the appraiser and the receiving charity.

When do you need a qualified appraisal for an artwork donation?

A qualified appraisal is required when you claim a federal income tax deduction for donated artwork valued over $5,000, whether a single piece or a group of similar items. At that threshold, IRS rules require a qualified appraiser's report attached to Form 8283 Section B to substantiate the deduction and avoid disallowance. Donations valued between $500 and $5,000 require only Form 8283 Section A, with no appraisal needed.

What credentials should the appraiser have?

The appraiser must be independent from both the donor and the charity, hold verifiable education and experience specific to the type of artwork being appraised, and comply with USPAP. The report must include a declaration of qualifications, a statement of no conflicts of interest, and fee disclosure. AppraiseItNow appraisers hold credentials through recognized professional organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB.

How is fair market value determined for donated artwork?

Fair market value is defined as the price a willing buyer and a willing seller would agree upon in an open market as of the exact donation date, consistent with IRS Publication 561. Appraisers support this conclusion using comparable sales, recent auction results, condition assessments, provenance, and authenticity documentation. For donors who held the work longer than one year, full fair market value generally applies, provided the charity uses the artwork for a related exempt purpose such as display.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are fully USPAP-compliant and prepared to meet IRS qualified appraisal standards, including proper valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration. For charitable donation purposes, our reports are structured specifically to satisfy IRS requirements for Form 8283 and audit substantiation.

How long does an artwork appraisal for charitable donation take?

Straightforward single-piece or small-collection assignments are typically completed in 5 to 7 days. More complex projects involving extensive provenance research, rare or difficult-to-compare works, or large collections generally take 2 to 3 weeks. We will give you a realistic timeline when we scope your assignment.

What does an artwork charitable donation appraisal cost?

Advanced appraisals prepared for IRS-qualified purposes such as charitable donations start at $395 per item, with a typical project range of $595 to $2,000 for standard assignments. Larger collections are priced by volume, with 10-item collections generally ranging from $2,200 to $15,000 and collections of 50 or more items starting around $12,000. Fees are quoted as a fixed price before work begins, and key cost factors include:

- Number of artworks being appraised

- Artist complexity and required market research depth

- Provenance and documentation quality

- Intended use and required IRS methodology

Visit our art appraisal page for more detail on scope and pricing.

Can you appraise artwork anywhere in the US?

Yes, AppraiseItNow provides artwork appraisals for clients across the entire United States. Many assignments are completed remotely using photographs, documentation, and provenance records you provide, with no geographic limitations on our service.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow appraisals are prepared to qualified appraisal standards, including a clearly stated valuation date, documented comparable sales methodology, appraiser credentials, and a non-contingent fee declaration, all of which are the core elements the IRS evaluates. While no appraiser can guarantee a specific outcome in an audit or legal proceeding, following these standards significantly reduces the risk of disallowance and positions your deduction as well-supported. Our reports are also structured to hold up in insurance and legal contexts where USPAP compliance is expected.

What happens if my donated artwork is valued over $20,000 or $50,000?

For donations over $20,000, the full qualified appraisal must be attached to Form 8283 on your tax return, along with high-resolution photographs if requested by the IRS. Claims exceeding $50,000 may be referred to the IRS Art Advisory Panel for additional scrutiny, which makes the strength of your comparable sales analysis and appraiser qualifications especially important. You may also optionally request a pre-filing IRS Statement of Value for added substantiation at that level.

Does the related use rule affect how much I can deduct for donated artwork?

Yes, the related use rule directly affects your deduction amount. If the charity plans to use the artwork for its exempt purpose, such as a museum displaying the piece, you can generally deduct the full fair market value. If the charity intends to sell the artwork immediately or use it in an unrelated way, your deduction is limited to your cost basis, and any appreciated value may be recaptured as income if the work is sold within three years without a related use certification.

When must the appraisal be signed relative to the donation date?

The qualified appraisal must be signed no earlier than 60 days before the donation date and no later than the due date of your tax return, including any extensions, for the year in which the deduction is first claimed. Signatures or dates outside that window invalidate the appraisal for IRS purposes. The valuation itself must reflect fair market value as of the exact date the donation was made.

Can a gallery expert or auction house specialist serve as the qualified appraiser?

An auction house or gallery specialist can qualify as the appraiser for IRS purposes, provided they are fully independent from both the donor and the charity and can document their specific expertise in the artwork type. The report must still include a declaration of qualifications, a conflict-of-interest statement, and full USPAP compliance. Lack of documented independence or credentials is one of the most common reasons the IRS rejects an otherwise well-prepared appraisal.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.