IRS-qualified vehicle appraisals for charitable donations, meeting Form 8283 requirements for FMV deductions over $5,000. AppraiseItNow provides USPAP-compliant fair market value reports for donated autos, helping donors maximize their deduction with full IRS documentation.

Best in class appraisers across asset types

.avif)

Joe Kattan

Jason Dolph, CAGA

Marnie Erkelens, CAGA

Aron Blue

Automobile Appraisals for Charitable Donation

When you donate a vehicle to a qualifying nonprofit, the IRS requires a qualified appraisal to support a fair market value deduction if the vehicle's value exceeds $5,000 and the charity plans to use it directly, make material improvements, or transfer it to a needy individual at below-market cost. Without meeting one of these exceptions, your deduction is limited to the charity's gross sale proceeds, which can be far below the vehicle's actual worth. AppraiseItNow's vehicle appraisal specialists prepare qualified appraisals that satisfy IRS Publication 561 requirements and support the completion of Form 8283 Sections A and B.

We deliver automobile charitable donation appraisals both online and onsite across the United States, working with donors to gather the documentation needed before the 60-day pre-donation deadline. Whether you need a single vehicle assessed or multiple donated cars that aggregate past the $5,000 threshold, our IRS charitable contribution appraisal services are structured to meet every regulatory requirement. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Vehicles We Appraise for Charitable Giving

AppraiseItNow appraises a wide range of automobiles donated to qualifying organizations, including:

- Passenger cars and sedans donated to nonprofits for direct program use

- Trucks and SUVs transferred to charities providing transportation services

- Classic and antique vehicles requiring specialized market comparables

- High-value luxury vehicles where FMV significantly exceeds likely auction proceeds

- Collector cars with documented provenance, restoration history, or limited production status

- Vehicles donated with material improvements made by the charity prior to valuation

- Fleet vehicles donated in groups that collectively exceed the $5,000 IRS threshold

- Hybrid and electric vehicles where residual value requires current market data

- Vehicles transferred below market to qualifying individuals as part of a charity's mission

- Specialty or modified vehicles that require condition-specific comparable sales analysis

How Our Automobile Charitable Donation Appraisal Process Works

- Appraisers gather vehicle-specific details including VIN, mileage, condition, ownership history, and any documented repairs or upgrades, then cross-reference current market data from comparable sales, dealer listings, and recognized valuation guides to establish a defensible fair market value.

- Each appraisal report is prepared to satisfy IRS qualified appraisal standards, including the appraiser's qualifications, the methodology used, and the factual basis for the concluded value, all formatted to support Form 8283 completion and attachment to your tax return.

- Appraisals are timed to fall within the IRS-required window, no earlier than 60 days before the donation date and no later than the due date of the tax return on which the deduction is claimed.

- AppraiseItNow's appraisers hold credentials through recognized professional organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB, and all work product is USPAP-compliant, providing the documentation needed to withstand IRS scrutiny.

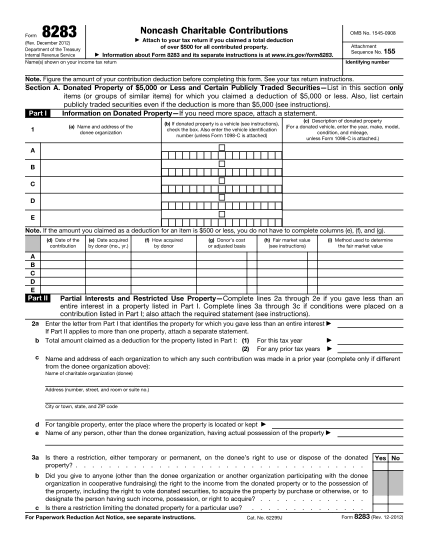

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does an Automobile appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does an automobile appraisal for charitable donation include?

An automobile appraisal for charitable donation is a written valuation that establishes the fair market value of your donated vehicle to support a federal tax deduction. The report includes a detailed vehicle description covering make, model, year, mileage, and condition, along with market data and comparable sales supporting the FMV conclusion. It is prepared to IRS standards per Publication 561 and attaches to Form 8283 Section B for tax substantiation.

When is a qualified appraisal required for a donated vehicle?

A qualified appraisal is required when you intend to claim a fair market value deduction exceeding $5,000 and the charity certifies significant intervening use, makes material improvements to the vehicle, or transfers it below market value to a needy individual. Without one of these exceptions, your deduction is generally limited to the gross proceeds the charity receives from selling the vehicle, as reported on Form 1098-C. The appraisal must be completed no more than 60 days before the donation date.

What credentials should the appraiser have?

The appraiser must meet IRS qualified appraiser standards: independent of both donor and donee, with demonstrated experience and training in automobile valuation, and operating under USPAP. Credentials from recognized organizations such as ASA, AAA, or specialty automotive appraisal groups are preferred and must be documented on Form 8283. For classic or specialty vehicles, specialized market knowledge is particularly important for IRS acceptance.

How is a donated vehicle's value determined for charitable donation purposes?

Appraisers establish fair market value using IRS Publication 561 methods, which center on comparable sales from auctions, dealer listings, and recognized guides such as NADA, adjusted for the vehicle's specific condition, mileage, mechanical state, and any provenance or improvements. Classic and specialty vehicles require comps drawn from relevant specialty markets rather than generic guides. The charity's certified intended use or improvements can support a full FMV deduction rather than a proceeds-limited one.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are fully USPAP-compliant and prepared to IRS qualified appraisal standards, including a defined valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration. Our appraisers hold credentials through recognized organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB. Following these standards significantly reduces the risk of IRS challenge or rejection.

How long does an automobile appraisal for charitable donation take?

Turnaround is typically 3 to 5 days depending on the complexity of the vehicle and the number of assets being appraised. Classic, modified, or limited-production vehicles may require additional research time. If you have a filing deadline approaching, contact us early so we can plan accordingly.

What does an automobile charitable donation appraisal cost?

Advanced automobile appraisals for charitable donation purposes, which must meet IRS qualified appraisal standards, start at $295 per vehicle. Typical fees for a single vehicle range from $195 to $495, while small fleets of around five vehicles generally run $795 to $1,500, and larger fleets of ten or more vehicles are priced at $1,800 to $4,500 or more with aggregate discounts applied. Factors that affect cost include vehicle complexity, condition analysis, documentation quality, and timeline needs. Visit our auto appraisal page for more detail, and note that all fees are quoted as a fixed price before work begins.

Can you appraise automobiles anywhere in the US?

Yes, AppraiseItNow provides automobile appraisals nationwide. Our appraisers serve clients across all 50 states, and our process is designed to work efficiently whether your vehicle is a single daily driver or part of a large collection.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow appraisals are prepared to IRS qualified appraisal standards, including a defined valuation date, documented FMV methodology with comparable sales, appraiser credentials, and a non-contingent fee declaration, all of which are the key requirements for Form 8283 substantiation. While no appraiser can guarantee acceptance in every situation, following these standards significantly reduces the risk of IRS challenge. The same report can also support insurance claims or legal proceedings where a credible, well-documented FMV conclusion is needed.

When exactly do I need an appraisal to claim the full fair market value of my donated car?

You need a qualified appraisal when your FMV deduction claim exceeds $5,000 and the charity certifies significant intervening use of the vehicle, such as using it regularly in their programs, makes material improvements, or transfers it below market value to a qualifying individual. Without one of these certified exceptions, the IRS limits your deduction to the charity's gross sales proceeds, which are often far below the vehicle's actual value. The appraisal must be completed no more than 60 days before the donation and attached to Form 8283 Section B.

What qualifies as significant intervening use by a charity, and why does it matter for my deduction?

Significant intervening use means the charity actively uses the vehicle in its programs for a substantial period, such as delivering meals or transporting clients, and certifies that use in a timely written acknowledgment with details on duration and purpose. This exception allows you to deduct the vehicle's full fair market value rather than the lower auction proceeds. Incidental activities like cleaning or painting the vehicle before sale do not qualify as significant use.

How should a classic car be valued for a charitable donation appraisal?

Classic cars must be valued at fair market value using specialized comparable sales from relevant auctions and dealer listings, adjusted for the vehicle's specific condition, mileage, provenance, upgrades, and regional market demand. Generic pricing guides alone are generally insufficient for IRS scrutiny on classic or specialty vehicles. Retaining maintenance records and working with an appraiser who has demonstrated classic car expertise strengthens the report's credibility.

What forms do I need for my car donation depending on the vehicle's value?

The required documentation scales with the claimed deduction:

- $250 to $500: written acknowledgment from the charity

- $501 to $5,000: Form 8283 Section A plus a charity letter with VIN, date, condition, and intended use or sale details

- Over $5,000 FMV claim: qualified appraisal plus Form 8283 Sections A and B with appraiser and charity signatures

Retain all records for at least three years, or seven years for deductions over $5,000.

Can the appraisal be completed more than 60 days before I donate the vehicle?

No. IRS rules require the appraisal to be completed no more than 60 days before the donation date. An appraisal performed outside that window does not qualify, and the FMV deduction over $5,000 would be disallowed. Plan ahead so the appraisal, donation, and any charity certifications all fall within the required timeframe.

What happens if the charity sells my donated car within two years after I claimed fair market value?

If the charity sells the vehicle within two years without completing the certified significant use or improvements that justified your FMV deduction, they are required to file Form 8282 with the IRS and send you a copy. This may require you to file an amended return and limit your deduction to the actual sales proceeds. Keeping records of the charity's certification and your appraisal is important in case of an audit.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.