IRS-qualified appraisals for donated floral arrangements, meeting Form 8283 requirements for contributions over $5,000. AppraiseItNow provides USPAP-compliant fair market value reports for charitable flower donations, giving donors the documentation needed to support their deduction with confidence.

Best in class appraisers across asset types

.avif)

Joe Kattan

Aron Blue

Flower Appraisals for Charitable Donations

Donating floral arrangements, rare botanical specimens, or large-scale event florals to a qualifying organization can generate a meaningful tax deduction, but the IRS requires a qualified appraisal when the donated flowers exceed $5,000 in value for a single item or group of similar items. The applicable standard is fair market value, defined as the price a willing buyer would pay a willing seller with neither under compulsion and both reasonably informed. Form 8283 Section B must be completed and signed by both the appraiser and the donee organization. AppraiseItNow's personal property appraisal services cover floral donations of all kinds, from ceremonial arrangements to rare horticultural collections.

We deliver appraisals both online and onsite across the United States, working with donors to document condition, provenance, and comparable market data as of the contribution date. Our charitable donation appraisals are completed within IRS timing requirements, no earlier than 60 days before the donation and no later than the tax return due date. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Types of Floral Donations We Appraise

AppraiseItNow appraises a wide range of floral property for charitable donation purposes, including:

- Large-scale event floral installations donated to nonprofits, museums, or cultural organizations

- Rare or exotic flower specimens with documented horticultural significance

- Ceremonial or culturally significant floral arrangements, such as those used in religious or traditional contexts

- Preserved or dried botanical collections with collectible or archival value

- Potted flowering plants or living botanical specimens donated to botanical gardens or educational institutions

- Silk or artificial floral arrangements with recognized decorative or antique value

- Floral artwork or pressed flower compositions framed and donated as decorative pieces

- Wholesale floral inventory donated by florists or event companies to qualifying charities

- Seasonal or holiday floral displays donated after use at corporate or institutional events

- Grouped donations of multiple arrangements that aggregate above the $5,000 IRS threshold

How Our Flower Appraisal Process Works

- Appraisers assess fair market value as of the exact contribution date, accounting for perishability, condition at the time of donation, rarity, and available comparable market data for similar floral property.

- Each report documents the item or group description, valuation methodology, comparable sales or market references, and the appraiser's qualifications, providing everything needed to support Form 8283 Section B.

- AppraiseItNow appraisers hold credentials through recognized professional organizations including ISA and AAA, meet IRS qualified appraiser standards, and have completed USPAP coursework required for charitable donation work.

- Appraisals are available online using photographs and documentation provided by the donor, or onsite when physical inspection is necessary to accurately assess condition and scale.

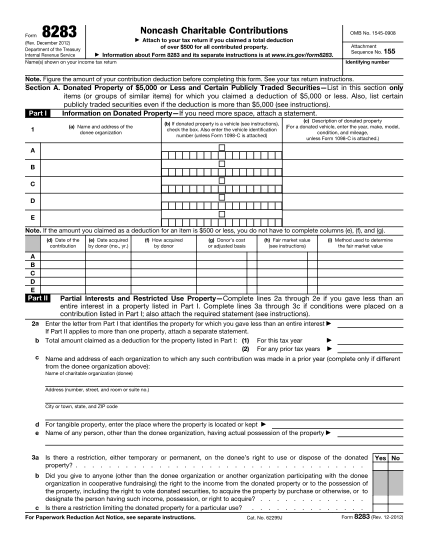

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does a Flower appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does a flower appraisal for charitable donation involve?

A flower appraisal for charitable donation determines the fair market value of floral arrangements or botanical items you are donating to a qualified charity, producing documentation that substantiates your tax deduction. The appraiser evaluates species, condition, arrangement complexity, artistic merit, and current market comparables to establish an objective, IRS-compliant value. The resulting report is prepared to qualified appraisal standards and supports the filing of IRS Form 8283.

When do you need a flower appraisal for a charitable donation?

A qualified appraisal is required when the total value of donated flower arrangements exceeds $5,000, whether as a single item or as a group of similar items that aggregate above that threshold. For donations valued between $500 and $5,000, you must complete IRS Form 8283 Section A but no formal appraisal is needed. Donations under $500 require only a written acknowledgment from the receiving charity.

What credentials should the appraiser have?

The appraiser must meet IRS qualified appraiser standards, meaning they cannot be the donor or donee, must have completed a 15-hour USPAP course plus 30 hours of appraisal education, and must have performed five or more appraisals in the prior five years. AppraiseItNow appraisers hold credentials through recognized organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB. For flower donations specifically, expertise in personal property and floral or horticultural valuation is important to properly address perishability and market-specific factors.

How is fair market value determined for donated flowers?

Flower appraisals follow the willing buyer and willing seller standard, meaning the price at which the flowers would change hands between two informed parties, neither under compulsion. Appraisers research comparable sales of similar floral arrangements and adjust for the donation date, species, condition, arrangement complexity, and scale. Because flower condition and seasonal pricing shift quickly, the appraisal must reflect value on the exact date of contribution.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are fully USPAP-compliant and prepared to IRS qualified appraisal standards, including proper valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration. This means the report is structured to satisfy the requirements for charitable donation deductions when attached to or retained with your tax filing.

How long does a flower appraisal take?

Most remote flower appraisals are completed in 7 to 10 days. Onsite inspections or larger collections typically take 2 to 3 weeks. Rush service is available for same-day or next-day turnaround if your filing deadline or donation timing requires it.

What does a flower appraisal for charitable donation cost?

Advanced appraisals for charitable donation purposes start at $495, with a typical range of $495 to $2,000 depending on the size and complexity of the collection. A small collection of one to a few items generally falls between $495 and $695, a medium collection of around ten items runs $695 to $1,200, and large collections can range from $1,200 to $3,500 or more. Fees are quoted as a fixed price before work begins, based on factors like item quantity, rarity, documentation quality, and desired turnaround. Visit our personal property appraisal page for more detail.

Can you appraise flowers anywhere in the US?

Yes, AppraiseItNow provides flower appraisals nationwide. Remote appraisals are conducted using photos and documentation you submit, and onsite inspections can be arranged across the country for larger or more complex collections.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow appraisals are prepared to qualified appraisal standards, including a defined valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration, all of which align with IRS requirements for noncash charitable contributions. While no appraiser can guarantee acceptance in every context, following these standards significantly reduces the risk of a deduction being denied or challenged. For insurance or legal matters, an IRS-compliant USPAP report provides credible, well-documented support for the stated value.

Do flower donations to multiple charities count together toward the $5,000 appraisal threshold?

Yes, similar flower items aggregate toward the $5,000 threshold even when donated to different organizations. If the combined value of similar floral arrangements exceeds $5,000, a qualified appraisal is required and a separate Form 8283 Section B must be filed for each donee. This aggregation rule applies regardless of whether the donations happen on the same date or to the same charity.

Can the appraisal be completed after I donate the flowers to the charity?

The appraisal must be completed no more than 60 days before the donation and no more than 30 days after it, and it must reflect the fair market value on the exact date of contribution. Because flower condition changes rapidly, an appraisal performed well after the donation may not accurately capture the value at the time of giving, which can jeopardize your deduction. The appraisal must also be completed before your tax return is due, including any extension period.

What goes on Form 8283 when donating a large event flower setup worth over $5,000?

For donations exceeding $5,000, you must complete Form 8283 Section B, which requires a detailed description of the flowers, the donation date, the appraised fair market value, the appraiser's signature and IRS qualification declaration, and the charity's acknowledgment. The appraiser certifies that the appraisal was prepared in compliance with USPAP and that they have no financial interest in the outcome. You attach the Form 8283 Section B summary to your tax return and retain the full appraisal report unless the value exceeds $500,000.

What is the most common mistake donors make when appraising flowers for a tax deduction?

The most frequent error is waiting too long to arrange the appraisal, resulting in flowers that have wilted or deteriorated before they are evaluated, which means the appraisal no longer reflects the fair market value on the actual donation date. A second common mistake is simply not obtaining a qualified appraisal at all for donations exceeding $5,000, which leads to the IRS denying the deduction entirely even if the flowers were genuinely valuable. Timing the appraisal correctly and working with a credentialed appraiser from the start protects your deduction.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.