IRS-qualified appraisals for donated RVs, meeting Form 8283 Section B requirements for claims over $5,000. AppraiseItNow provides USPAP-compliant fair market value reports with comparable sales analysis, giving donors a defensible deduction.

Best in class appraisers across asset types

.avif)

Joe Kattan

Aron Blue

RV Appraisals for Charitable Donation

When you donate a recreational vehicle to a qualifying nonprofit, the IRS requires a qualified appraisal to substantiate any deduction claimed at $5,000 or more. This appraisal must establish the fair market value of the RV as of the contribution date, and the completed report must support Form 8283 Section B, signed by both the appraiser and the receiving organization. AppraiseItNow's vehicle appraisal practice handles this process for all RV types, from Class A motorhomes to vintage travel trailers, with reports built to meet IRS documentation standards.

We deliver appraisals both online and onsite across the United States, making it straightforward to meet your filing deadline regardless of where the RV is located. Our IRS-qualified charitable donation appraisals are completed by credentialed appraisers with direct experience valuing recreational vehicles in the current market. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

RVs We Appraise for Charitable Giving

AppraiseItNow covers the full range of recreational vehicles commonly donated to nonprofits, faith organizations, and charitable programs.

- Class A motorhomes, including diesel pushers and gas-powered coaches

- Class B camper vans and Class C motorhomes

- Super C motorhomes built on commercial truck chassis

- Fifth wheel trailers, including luxury and toy hauler configurations

- Conventional travel trailers ranging from entry-level to high-end models

- Pop-up folding campers and hybrid trailers

- Truck campers, both slide-in and non-slide models

- Teardrop trailers and compact specialty campers

- Park model RVs used for recreational purposes

- Vintage, restored, or heavily customized RVs with non-standard market comparables

How AppraiseItNow Handles RV Charitable Donation Appraisals

Our process is built around the specific documentation and timing requirements the IRS imposes on vehicle donations.

- Appraisals are completed within the IRS-required window: no earlier than 60 days before the donation date and no later than the tax return due date, including extensions

- Each report documents the RV's condition, mileage, features, ownership history, and relevant upgrades, supported by comparable market sales data adjusted for the contribution date

- The final report is formatted to support Form 8283 Section B and includes the appraiser's qualifications, methodology, and certification as required for a qualified appraisal under IRS guidelines

- All appraisers hold credentials from recognized professional organizations including ISA, ASA, AAA, CAGA, AMEA, or NEBB, and all reports are prepared in full compliance with USPAP

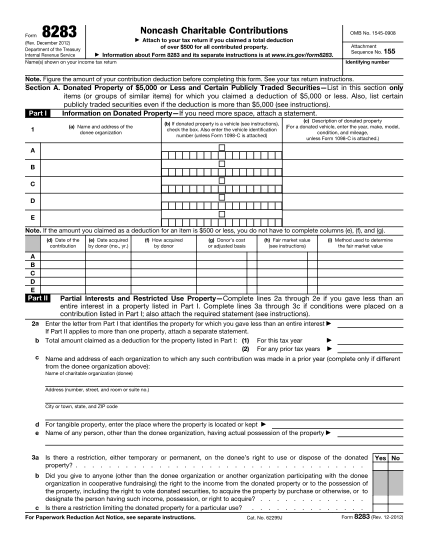

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does a Recreational Vehicle appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does an RV appraisal for a charitable donation involve?

A charitable donation appraisal for a recreational vehicle determines the fair market value of the RV as of the donation date, using comparable sales adjusted for condition, mileage, and current market data. The report includes photographs, comparable sales documentation, and a detailed written analysis formatted to support IRS Form 8283 for deductions over $5,000. The process is fully USPAP-compliant and prepared by a credentialed appraiser with no financial interest in the transaction.

When do you need a qualified appraisal for an RV donation?

A qualified appraisal is required when you claim a deduction of $5,000 or more in fair market value for a donated RV. The threshold can also be triggered by aggregation, meaning if you donate multiple similar items such as vehicles totaling over $5,000 in a tax year, even across different charities, a qualified appraisal is required. If the charity sells the RV and issues Form 1098-C, your deduction may be limited to sale proceeds, but exceptions apply for significant use or material improvements.

What credentials should the appraiser have?

The IRS requires a qualified appraiser who holds a recognized designation from an organization such as ISA, ASA, AAA, or a comparable credentialing body, has relevant experience appraising recreational vehicles, and has no conflict of interest with the donor or charity. AppraiseItNow appraisers are credentialed through ISA, ASA, AAA, CAGA, AMEA, and NEBB, and all appraisals are USPAP-compliant. RV-specific expertise is essential for accurate condition assessment and proper comparable selection.

How is a recreational vehicle valued for charitable donation purposes?

Appraisers determine fair market value using the price a willing buyer and willing seller would agree upon in an arm's-length transaction as of the donation date. Comparable sales of similar make, model, year, and class of RV are analyzed and adjusted for mileage, mechanical condition, interior and exterior wear, upgrades, and maintenance history. Market conditions, geographic factors, and IRS Publication 561 guidelines all inform the final value conclusion.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are prepared in compliance with the Uniform Standards of Professional Appraisal Practice. For charitable donation purposes, our reports are structured to meet IRS qualified appraisal requirements, including a stated valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration. This significantly reduces the risk of IRS scrutiny or report rejection.

How long does a Recreational Vehicle appraisal take?

Turnaround is typically 3 to 5 days depending on the complexity of the vehicle and the number of assets being appraised. More specialized or modified RVs, or assignments involving multiple units, may require additional time for thorough research and documentation. We will confirm the expected timeline when scoping your assignment.

What does an RV charitable donation appraisal cost?

Advanced RV appraisals for charitable donation purposes start at $295, reflecting the IRS-qualified report requirements for this use. The typical range for a single RV is $195 to $495, with volume pricing available for fleets of 5 or more vehicles. Cost factors include the RV's complexity, condition analysis needed, documentation quality, and timeline requirements. Visit our auto appraisal page for more detail, and note that all fees are quoted as a fixed price before work begins.

Can you appraise recreational vehicles anywhere in the US?

Yes, AppraiseItNow provides RV appraisals nationwide. Our appraisers work across all 50 states, and our process is designed to accommodate donors and organizations regardless of location.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow appraisals are prepared to qualified appraisal standards, including a stated valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration, all of which align with IRS requirements for charitable donation deductions over $5,000. While no appraiser can guarantee acceptance in every circumstance, following these standards significantly reduces the risk of rejection or audit challenge. Insurers and courts also generally recognize USPAP-compliant reports prepared by credentialed appraisers.

When exactly must the appraisal be completed relative to my donation date?

The IRS requires that the appraisal be completed no earlier than 60 days before the donation date and no later than the due date of your tax return, including any extensions. The report must state the fair market value as of the actual contribution date. Planning ahead ensures you meet this window without rushing the appraisal process.

What happens if the charity sells my donated RV shortly after receiving it?

If the charity sells the RV, your deduction is generally limited to the gross proceeds reported on Form 1098-C, which the charity must provide within 30 days of the sale. In that scenario, a qualified appraisal may not be required to support the proceeds-based deduction. However, if you qualify for an exception, such as the charity making significant improvements to the RV or using it substantially for its exempt purpose, a qualified appraisal is still needed to claim fair market value.

How do mileage and condition affect my RV's fair market value for a donation deduction?

Mileage and physical condition are among the most significant factors in determining an RV's fair market value, as they reflect mechanical wear, interior and exterior deterioration, and overall desirability in the resale market. Appraisers compare the subject RV against similar units sold around the donation date and apply adjustments for these variables. Poor condition or high mileage will reduce the appraised value relative to cleaner, lower-mileage comparables.

Can donating multiple RVs in one tax year push me over the $5,000 appraisal threshold?

Yes, the IRS aggregates similar items donated in the same tax year, and recreational vehicles are treated as similar property. If the combined fair market value of all donated RVs exceeds $5,000, a qualified appraisal is required even if each individual vehicle is valued below that threshold. This rule applies even when donations are made to different charitable organizations throughout the year.

Does Form 8283 need to be signed by the appraiser and the charity?

Yes, for noncash charitable contributions over $5,000, you must attach a completed Form 8283 Section B to your tax return, and it requires signatures from you as the donor, the qualified appraiser, and an authorized representative of the donee organization. The appraiser's signature confirms their qualifications and the independence of the appraisal. Missing signatures are a common reason the IRS disallows deductions, so coordinating this step before filing is important.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.