IRS-qualified appraisals for donated machinery and equipment, meeting the Form 8283 Section B threshold above $5,000. AppraiseItNow provides USPAP-compliant fair market value reports that protect your deduction and satisfy IRS documentation requirements.

Best in class appraisers across asset types

.avif)

Joe Kattan

Jason Dolph, CAGA

Marnie Erkelens, CAGA

Aron Blue

Equipment and Machinery Appraisals for Charitable Donations

When a business or individual donates equipment or machinery to a qualifying nonprofit, the IRS requires a qualified appraisal if the claimed deduction exceeds $5,000. That appraisal must establish the fair market value of the donated assets and support the completion of Form 8283 Section B, which both the appraiser and the donee organization must sign. Our equipment valuation practice covers the full range of industrial, commercial, and specialized machinery that businesses commonly donate to schools, vocational programs, nonprofits, and other qualified organizations.

AppraiseItNow delivers these valuations both online and onsite across the United States, working with donors to meet the IRS timing requirement that appraisals be completed no earlier than 60 days before the donation date. Whether you need a single machine valued or an entire facility's worth of assets assessed, our charitable donation appraisal services are built to produce documentation that holds up to IRS scrutiny. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Equipment and Machinery We Appraise for Charitable Giving

AppraiseItNow appraises a wide variety of tangible assets donated to qualifying organizations, including:

- Manufacturing and production equipment such as CNC machines, lathes, and milling equipment

- Construction equipment including excavators, bulldozers, forklifts, and aerial lifts

- Agricultural machinery such as tractors, combines, irrigation systems, and tillage equipment

- Medical and dental equipment including imaging devices, surgical tools, and diagnostic instruments

- Restaurant and commercial kitchen equipment such as ovens, refrigeration units, and prep stations

- Printing and publishing equipment including offset presses, bindery machines, and large-format printers

- Woodworking and fabrication equipment such as saws, routers, and welding systems

- IT and data center hardware including servers, networking equipment, and storage arrays

- Vehicles and fleet assets used in commercial operations, including trucks, vans, and specialty vehicles

- Laboratory and scientific instruments such as spectrometers, centrifuges, and testing equipment

How AppraiseItNow Handles Equipment Donation Appraisals

Our appraisers hold credentials through recognized professional organizations including ASA, AMEA, and NEBB, with specific expertise in machinery and equipment valuation rather than general personal property.

- Each appraisal report documents the asset's condition, age, remaining useful life, and comparable market data, providing the factual foundation the IRS expects to see when reviewing Form 8283 submissions.

- Appraisers assess whether the equipment is general-purpose or highly specialized, since specialized machinery often has a narrower resale market that directly affects fair market value conclusions.

- The completed report satisfies USPAP standards and includes all information required for the appraiser to sign Section B of Form 8283, including the appraiser's qualifications, the valuation methodology used, and the effective date of the appraisal.

- Appraisals are available for single assets or large multi-item donations, with turnaround options designed to meet tax filing deadlines without sacrificing accuracy or defensibility.

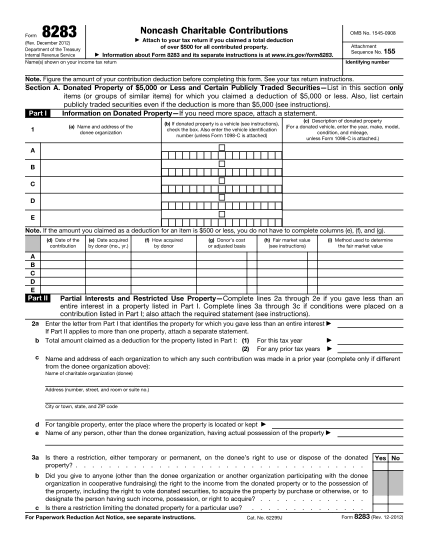

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does an Equipment & Machinery appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does an equipment and machinery appraisal for charitable donation involve?

This type of appraisal establishes the fair market value of donated machinery or equipment for IRS tax deduction purposes. The appraiser analyzes the asset's condition, age, remaining useful life, and comparable market sales data, then produces a USPAP-compliant written report. The report supports IRS Form 8283 and provides the documentation needed to substantiate your claimed deduction.

When is a charitable donation appraisal required for equipment?

An appraisal is required when the claimed value of donated equipment or machinery exceeds $5,000 to a qualified 501(c)(3) organization. If you are donating similar items that each fall below $5,000 but collectively exceed that threshold, an appraisal is still required. Dissimilar items each valued below $5,000 do not trigger this requirement.

What credentials should the appraiser have?

The appraiser must hold professional credentials in equipment, machinery, or tangible personal property valuation, such as those issued by ISA, ASA, AAA, CAGA, AMEA, or NEBB. They must follow USPAP standards and have specific experience with IRS charitable donation rules, including the ability to sign Section B of Form 8283 as a qualified appraiser. Expertise in machinery markets and depreciation analysis is essential for a defensible report.

How is fair market value determined for donated equipment and machinery?

Fair market value reflects the price a willing buyer would pay a willing seller in an open market, with both parties fully informed and under no pressure to complete the transaction. Appraisers evaluate the equipment's age, condition, wear, functional utility, and remaining useful life, then compare it against actual market sales data. For specialized machinery with limited resale markets, appraisers may also apply a cost approach to arrive at a supportable value.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are prepared in full compliance with the Uniform Standards of Professional Appraisal Practice. Each report includes a defined valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration, which are the core elements the IRS looks for in a qualified appraisal. Our credentialed appraisers are experienced with charitable donation assignments specifically.

How long does an equipment and machinery appraisal take?

Most remote appraisals are completed in 7 to 10 days. Onsite inspections or larger equipment collections typically take 2 to 3 weeks. Rush service is available for same-day or next-day turnaround if your donation timeline requires it.

What does a charitable donation appraisal for equipment and machinery cost?

Fees are quoted as a fixed price before work begins, so there are no surprises. Single-item appraisals start at $395 for IRS-qualified reports, and most equipment and machinery appraisals fall in the range of $695 to $3,000 depending on the number of items, technical complexity, condition differences, and whether an onsite inspection is needed. Larger inventories of 50 or more items may run $5,000 to $10,000 or more. Visit our equipment appraisal page for more detail on what drives cost.

Can you appraise equipment and machinery anywhere in the US?

Yes, AppraiseItNow provides equipment and machinery appraisals nationwide. Remote appraisals can be completed using photos, serial numbers, specifications, and maintenance records submitted by the client. For larger collections or assets requiring physical inspection, our appraisers can conduct onsite visits across the country.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow prepares charitable donation appraisals to meet the IRS definition of a qualified appraisal, including a defined valuation date, documented methodology, appraiser credentials, and a non-contingent fee structure. While no appraiser can guarantee acceptance in every audit or legal proceeding, following these standards significantly reduces the risk of disallowance. Our reports are also prepared to professional standards that hold up in insurance and legal contexts.

Does the holding period for my equipment affect the deduction amount?

Yes, the length of time you have owned the equipment affects how your deduction is calculated. If you have held the machinery for more than one year, your deduction is generally the full fair market value, subject to AGI limits. If held for one year or less, the deduction is limited to the lesser of fair market value or your adjusted cost basis.

What IRS forms and documentation are required when donating equipment?

For equipment donations valued over $5,000, you must file IRS Form 8283 Section B, signed by your qualified appraiser, and attach the qualified appraisal report to your tax return. If the donation value exceeds $500,000, the full appraisal must be included with your return rather than kept on file separately. You should also retain the charity's written acknowledgment and all supporting records in case of an audit.

When must the appraisal be completed relative to the donation date?

The IRS requires that the appraisal be completed no more than 60 days before the effective donation date, which is typically when title transfers to the charity. Appraisals completed earlier than that window risk disallowance, so coordinating timing with your appraiser before the transfer is important. Planning ahead ensures the report reflects the equipment's condition at the time of the gift.

Can leased equipment be donated for a charitable tax deduction?

No, leased equipment does not qualify for a charitable donation deduction because you must own the asset outright to transfer it. Leased machinery remains the property of the lessor, and donating it could also violate the terms of your lease agreement. Clear documentation of ownership is a prerequisite before an appraisal for charitable donation purposes can be completed.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.