IRS-qualified boat appraisals for charitable donations, meeting the Form 8283 and Form 1098-C requirements. AppraiseItNow provides USPAP-compliant fair market value reports for donated vessels, giving donors the documentation needed to support their deduction.

Best in class appraisers across asset types

.avif)

Joe Kattan

Marnie Erkelens, CAGA

Aron Blue

Boat Appraisals for Charitable Donations

Donating a boat to a qualified organization can generate a meaningful tax deduction, but the IRS has specific requirements that must be met before you can claim it. For boats valued at $5,000 or more, a qualified appraisal is required, and the appraiser must meet IRS credential standards, have no conflicts of interest, and complete the appraisal within a defined window: no earlier than 60 days before the donation and no later than your tax return due date. The IRS standard for this type of appraisal is fair market value, defined as the price a willing buyer and seller would agree on with no compulsion and full knowledge of the relevant facts. Our marine vessel appraisal team provides credentialed, USPAP-compliant reports that satisfy these requirements and support Form 8283 Section B.

AppraiseItNow delivers appraisals both online and onsite across the United States, making it straightforward to meet IRS deadlines regardless of where the vessel is located. Our IRS charitable contribution appraisals include a fully documented report with appraiser credentials, methodology, comparable market data, and the signed appraiser declaration required on Form 8283. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Types of Boats We Appraise for Charitable Giving

AppraiseItNow appraises a wide range of vessels for donation purposes, including:

- Powerboats and runabouts, including bowriders, deck boats, and cuddy cabins

- Sailboats, from daysailers and sloops to offshore cruising vessels

- Pontoon boats and tritoons

- Fishing boats, including bass boats, bay boats, and offshore sportfishing vessels

- Personal watercraft such as jet skis and wave runners

- Houseboats and liveaboard vessels

- Inflatable and rigid inflatable boats (RIBs)

- Vintage and classic boats requiring specialized market knowledge

- Boats with significant marine electronics packages, outboard motors, or trailer packages included in the donation

- Commercial and charter vessels being donated to qualifying nonprofit organizations

How Our Boat Appraisal Process Works for Donations

Our appraisers hold credentials from recognized professional organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB, and bring direct experience valuing marine vessels across a range of types, ages, and market conditions.

- The appraisal report documents the vessel's make, model, year, hull condition, engine hours, installed equipment, and any accessories included in the donation, along with the methodology used to determine fair market value.

- Comparable sales data, marine pricing guides, and regional market conditions are all considered in reaching a supportable value conclusion, which is particularly important given that boat values can vary significantly by season and geography.

- The completed report includes the appraiser's signed declaration as required for Form 8283 Section B, and is formatted to meet IRS qualified appraisal standards so your tax preparer can attach it directly to your return.

- Clients should be aware that for boat donations where the charity sells the vessel, the IRS generally limits the deduction to the gross proceeds reported on Form 1098-C rather than the appraised fair market value, and our appraisers can explain how this interacts with the appraisal requirement during the engagement.

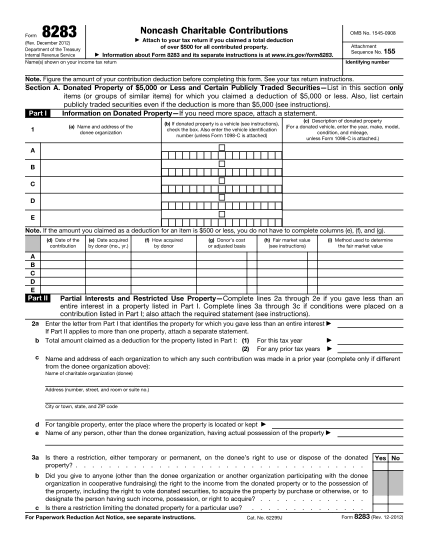

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does a Boat appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does a charitable donation boat appraisal involve?

A charitable donation boat appraisal is a formal evaluation of your vessel's fair market value, conducted by a credentialed appraiser to substantiate your tax deduction when donating to a qualified charity. The process includes a review of the boat's condition, age, make, model, engine hours, marine electronics, and comparable market sales. The resulting report is prepared to IRS qualified appraisal standards and supports your filing on Form 8283.

When do you need a qualified appraisal for a donated boat?

A qualified appraisal is required when your claimed deduction for a donated boat exceeds $5,000. For donations between $500 and $5,000, you still need documented fair market value and Form 8283 Section A, though a full qualified appraisal is not mandatory. If the charity sells the boat rather than using it directly, your deduction is generally capped at the gross proceeds reported on Form 1098-C, regardless of the appraised value.

What credentials should the appraiser have?

The appraiser should hold recognized professional designations from organizations such as the American Society of Appraisers, the International Society of Appraisers, or similar credentialing bodies, along with demonstrated experience valuing boats and marine assets. They must have no financial interest in the transaction and no conflicts of interest with either the donor or the charity. Marine-specific expertise covering hull condition, engine systems, and regional market dynamics is essential for an accurate and IRS-defensible opinion of value.

How is a donated boat's value determined?

Appraisers determine fair market value using the price a willing buyer and willing seller would agree upon in an open market, without compulsion. Key factors include hull integrity, engine hours, interior condition, marine electronics such as GPS and radar units, age, make, model, maintenance history, and recent comparable sales data. Regional and seasonal market conditions are also considered, and the valuation is anchored to the date of contribution.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are fully USPAP-compliant and prepared by credentialed appraisers affiliated with recognized professional organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB. For charitable donation purposes, our reports are structured to meet IRS qualified appraisal requirements, including proper valuation date, methodology disclosure, appraiser credentials, and a non-contingent fee declaration.

How long does a boat appraisal take?

Standard boat appraisals for charitable donation purposes are typically completed within 3 to 5 days. If a marine survey is required as part of the process, scheduling and completing that survey generally takes 3 to 5 weeks. We recommend initiating the appraisal well in advance of your donation date to ensure the report is ready before your tax return due date.

How is pricing structured for a charitable donation boat appraisal?

Charitable donation boat appraisals are classified as advanced-purpose appraisals, starting at $295, because they must meet IRS qualified appraisal standards. The typical fee range for boat appraisals runs from $195 to $495 for a single vessel, with factors such as specialty or vintage models, condition complexity, documentation quality, and timeline affecting the final quote. All fees are fixed and quoted before work begins, so there are no surprises. Visit our boat appraisal page for more detail on scope and pricing.

Can you appraise boats anywhere in the US?

Yes, AppraiseItNow provides boat appraisals nationwide. Our network of credentialed appraisers covers all regions of the country, and we can accommodate both in-person and desktop appraisal formats depending on the scope of your assignment.

Will my appraisal be accepted by the IRS, insurers, or courts?

Our appraisals are prepared to qualified appraisal standards, including a defined valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration, all of which align with IRS requirements outlined in Publication 561 and the instructions for Form 8283. While no appraiser can guarantee acceptance by any authority, following these standards significantly reduces the risk of challenge or disallowance. Insurers and courts may also rely on our USPAP-compliant reports, though acceptance in those contexts depends on the specific case and jurisdiction.

What is the IRS value threshold that triggers a qualified appraisal for a boat donation?

The IRS requires a qualified appraisal when the claimed deduction for a donated boat exceeds $5,000. For deductions between $500 and $5,000, fair market value documentation and Form 8283 Section A are required, but a full qualified appraisal is not. When multiple similar items are donated in the same tax year, the IRS may aggregate their values when applying these thresholds.

Why is my deduction limited to sales proceeds when I donate a boat?

IRS rules for donated vehicles, boats, and aircraft generally cap the deduction at the gross proceeds the charity receives from selling the vessel, not the donor's estimated fair market value. The charity is required to provide Form 1098-C within 30 days of the sale, and that figure becomes the basis for your deduction. An exception applies when the charity uses the boat directly for its mission rather than selling it, in which case fair market value may be deductible with proper substantiation.

When must the appraisal be completed relative to the donation date?

The qualified appraisal must be completed no earlier than 60 days before the donation date and no later than the due date of the tax return on which you claim the deduction. The written report must be in your possession before that return is filed. This timing requirement ensures the valuation reflects fair market value as of the actual contribution date.

What documentation supports a boat donation valued between $500 and $5,000?

For donations in this range, you should gather appraisal guide references, comparable sales data, professional marine surveyor reports if available, photographs, maintenance records, and acquisition details. A written acknowledgment from the charity is mandatory, and Form 8283 Section A must be completed and filed with your return. Keeping thorough records of all valuation methods used will strengthen your position if the IRS requests substantiation.

What boat-specific factors most affect charitable donation value?

The most influential factors include hull integrity, engine hours, signs of blistering or structural damage, interior condition, and the presence of marine electronics such as GPS units, radar, and fish finders, which are documented and valued separately. Age, make, model, documented upgrades, and provenance all contribute to the final opinion of value. Regional market conditions and the time of year can also shift fair market value meaningfully, particularly for seasonal watercraft.

What forms are required to claim a tax deduction on a donated boat over $5,000?

You will need Form 8283 Section B with the qualified appraisal attached and signed by the appraiser, as well as Form 1098-C from the charity if the boat is sold. Supporting documentation should include the donation acknowledgment letter, your cost basis records, and evidence of the appraiser's qualifications. These materials are filed alongside your itemized deductions on Schedule A of Form 1040.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.