IRS-qualified coin appraisals for charitable donations, meeting Form 8283 Section B requirements over $5,000. AppraiseItNow provides USPAP-compliant fair market value reports grounded in auction comparables and numismatic grading, protecting your deduction at filing.

Best in class appraisers across asset types

.avif)

Joe Kattan

Aron Blue

Coin Appraisals for Charitable Donations

When you donate a coin collection or individual numismatic pieces to a qualifying organization, the IRS requires a qualified appraisal to substantiate any deduction exceeding $5,000 in fair market value for similar items. Coins are not treated as readily valued property, so exchange quotes or dealer estimates do not satisfy this requirement. The appraisal must be completed no earlier than 60 days before the donation date and no later than your tax return due date, with Form 8283 Section B signed by both the appraiser and the donee. Our personal property appraisal services cover the full range of numismatic and bullion holdings donors commonly contribute to museums, historical societies, and other nonprofits.

AppraiseItNow delivers coin appraisals both online and onsite across the United States, working with donors who need a defensible, IRS-compliant report before filing. Whether you have a single rare coin or a multi-decade collection, our charitable donation appraisals are prepared by credentialed appraisers with the numismatic expertise to support your deduction. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Coins We Appraise for Charitable Giving

AppraiseItNow appraises a wide range of coin types commonly donated to qualifying organizations, including:

- U.S. rare and key-date coins, including early American copper, silver, and gold issues

- Modern and classic commemorative coins issued by the U.S. Mint

- Foreign and world coins, including ancient, medieval, and colonial-era pieces

- Proof and uncirculated sets in original government packaging

- Error coins and die varieties with documented numismatic significance

- Bullion coins such as American Gold Eagles, Silver Eagles, and Maple Leafs

- Certified coins graded and slabbed by PCGS or NGC

- Raw, ungraded coins requiring condition assessment as part of the appraisal

- Coin collections assembled by theme, date, or series, appraised as a group

- Estate coin accumulations with mixed types, conditions, and origins

How Our Coin Appraisal Process Works

- Appraisers analyze each coin's type, date, mint mark, condition, and provenance, referencing recent comparable auction results and PCGS/NGC population data to establish fair market value as of the donation date.

- The written appraisal report includes a detailed description of each item, the valuation methodology, comparable sales used, and the appraiser's signed declaration, giving you everything needed to complete Form 8283 Section B and attach supporting documentation to your return.

- For collections with multiple coins donated to a single organization on the same date, a single appraisal report can cover all items, with the appraiser signing per item on Form 8283 as required by IRS guidelines.

- AppraiseItNow's credentialed appraisers hold designations through recognized professional organizations including ISA, ASA, and AAA, and all appraisals are completed in full compliance with USPAP and IRS qualified appraisal standards under IRC Section 170(f)(11)(C).

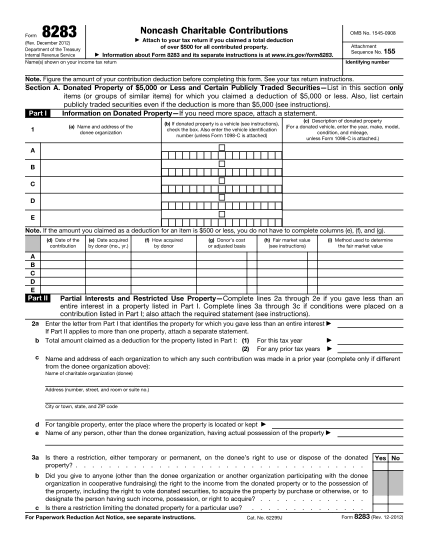

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does a Coins appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does a coins appraisal for charitable donation involve?

A charitable donation coins appraisal determines the fair market value of your coins or collection as of the donation date, using comparable auction sales, condition grades, rarity, mintage data, and current market trends. The resulting report is a qualified appraisal under IRS rules, prepared in compliance with USPAP, and includes detailed descriptions, photographs, and the appraiser's signed declaration. It supports your deduction claim on Form 8283 Section B for noncash contributions exceeding $5,000.

When do you need a coins appraisal for a charitable donation?

A qualified appraisal is required when the aggregate fair market value of similar donated items, meaning all coins combined, exceeds $5,000 on your tax return, even if no single coin reaches that threshold. This applies regardless of whether you donate to one charity or several, and regardless of how many separate donation dates are involved. The appraisal must be completed no earlier than 60 days before the donation and no later than the due date of your return, including extensions.

What credentials should the appraiser have?

The appraiser must meet IRS qualified appraiser standards, which include verifiable experience appraising coins, independence from the donor and donee, and compliance with USPAP. AppraiseItNow appraisers hold credentials through recognized professional organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB. They are also required to sign Form 8283 declaring their qualifications and confirming their fee is not contingent on the appraised value.

How are coins valued for charitable donation purposes?

Coins are valued at their fair market value as of the donation date, defined as the price a willing buyer and seller would agree upon with full knowledge of the relevant facts. Appraisers analyze recent auction comparables for identical or similar coins, adjusted for condition using the Sheldon scale, mint mark, year, rarity, provenance, and PCGS or NGC population reports. Dealer quotes and price guides alone are not sufficient substitutes for this analysis under IRS rules.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are fully USPAP-compliant and prepared to IRS qualified appraisal standards, including proper valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration. For charitable donation purposes, this means your report is structured to satisfy the requirements of IRC Section 170 and IRS Publication 561. While no appraisal firm can guarantee IRS acceptance, following these standards significantly reduces the risk of a challenge or disallowance.

How long does a coins appraisal take?

Most remote coins appraisals are completed within 7 to 10 days. Onsite inspections or larger collections typically take 2 to 3 weeks. Rush service is available for same-day or next-day turnaround if your donation deadline or tax filing date requires it.

What does a coins appraisal for charitable donation cost?

Advanced appraisals for charitable donation purposes, which require an IRS-qualified report, start at $295 for a single item. Typical project fees range from $595 to $2,200, and larger collections of 50 to 100 or more items generally fall between $1,500 and $6,000 or more with volume-based pricing. Fees depend on the number of coins, their complexity, and the quality of existing documentation. AppraiseItNow provides a fixed fee quote before work begins, so you know your cost upfront. Visit our personal property appraisal page for more detail.

Can you appraise coins anywhere in the US?

Yes, AppraiseItNow provides coins appraisals nationwide. Remote appraisals are conducted using photographs, documentation, and provenance materials you submit, making the process accessible regardless of your location. For larger or more complex collections, onsite inspection can also be arranged across the country.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow prepares charitable donation appraisals to meet IRS qualified appraisal standards, including proper valuation date, documented comparable sales methodology, appraiser credentials, and a non-contingent fee declaration signed on Form 8283. These elements are specifically designed to satisfy IRS requirements under IRC Section 170 and significantly reduce the risk of disallowance. No appraisal firm can guarantee acceptance in every case, but a properly prepared qualified appraisal is your strongest protection against a challenge.

If I donate a coin collection worth $8,000 total but each individual coin is worth less than $5,000, do I still need an appraisal?

Yes, because the IRS looks at the aggregate fair market value of similar items on your tax return, not the value of each individual piece. Since all coins are considered similar property, a total exceeding $5,000 triggers the qualified appraisal requirement and Form 8283 Section B, regardless of individual coin values. The fact that no single coin crosses the threshold does not exempt the group from this rule.

What is the difference between a coin dealer's quote and a qualified appraisal for my tax deduction?

A dealer's quote reflects a wholesale bid or retail ask price for a transaction, which is not the same as fair market value under IRS standards. A qualified appraisal determines FMV using comparable sales, condition analysis, and USPAP-compliant methodology, and it must be documented in a formal report with the appraiser's signed declaration. For deductions over $5,000, the IRS does not accept dealer quotes as a substitute, and relying on them risks disallowance with no reasonable cause exception.

Can I use PCGS or NGC price guides and recent auction results instead of hiring an appraiser?

Price guides and auction records are valuable data sources, but they cannot replace a qualified appraisal for deductions over $5,000. Coins are not considered readily valued property under IRC Section 170(f)(11), so the IRS requires a formal USPAP-compliant report with a signed appraiser declaration rather than self-valuation based on published guides. A qualified appraiser will incorporate that market data into the analysis, but the report itself is what satisfies the legal requirement.

If I donate coins to multiple charities on different dates, how do I know when to combine their values for the $5,000 threshold?

The IRS requires you to aggregate the fair market value of all similar items, meaning all coins, across all donees and all donation dates when calculating whether the $5,000 threshold is met on your return. If the combined total exceeds $5,000, a qualified appraisal is required even if each individual donation was below that amount. A single appraisal report can cover multiple donations, with the appraiser signing a separate Form 8283 Section B for each donee as needed.

What specific information about my coins must the appraiser include in the report for the IRS to accept my deduction?

The report must contain a detailed inventory covering each coin's quantity, type, year, mint mark, condition grade, metal content, distinguishing characteristics, and photographs. It must also include the fair market value per item and in total, a comparable sales analysis, the appraiser's qualifications and signature, and confirmation that the appraisal was completed within the required timing window. Form 8283 Section B must be signed by both the appraiser and the donee organization, and the full report must be attached to your return if the claimed deduction exceeds $500,000.

How much does a coin's condition grade affect the fair market value assigned for my donation deduction?

Condition grade has a significant impact on fair market value in numismatics, where even minor wear can reduce a coin's value substantially. An MS-70 coin in perfect uncirculated condition commands a far higher price than the same coin graded VF-30 with visible wear, and appraisers use PCGS and NGC population data alongside auction comparables to calibrate that difference precisely. The appraised FMV reflects what a willing buyer would pay for that specific coin in that specific grade on the donation date.

If the IRS challenges my appraised value and determines my coins are worth less, what happens to my deduction?

Your deduction would be reduced to the IRS-determined fair market value, and any tax underpayment resulting from the disallowed portion may be subject to accuracy-related penalties of 20 to 40 percent depending on the degree of overvaluation. A qualified appraisal prepared to IRS standards reduces but does not eliminate the risk of a challenge, and maintaining thorough documentation supports your position if one occurs. Substantial or gross valuation misstatements carry the steepest penalties, so working with a credentialed appraiser from the outset is the most effective way to protect your deduction.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.