IRS-qualified jewelry appraisals for charitable donations, meeting Form 8283 Section B requirements. AppraiseItNow provides fair market value reports for rings, gemstones, watches, and estate pieces to support your deduction with confidence.

Best in class appraisers across asset types

.avif)

Joe Kattan

Aron Blue

Jewelry Appraisals for Charitable Donations

When you donate jewelry to a qualifying nonprofit and plan to claim a tax deduction, the IRS requires a qualified appraisal if the claimed value exceeds $5,000 per item or group of similar items. That appraisal must establish fair market value as of the donation date and must be completed no earlier than 60 days before the gift is made. Form 8283 Section B must be signed by both the appraiser and the donee organization. AppraiseItNow's personal property appraisal services cover the full spectrum of fine jewelry, from single heirloom pieces to large donated collections.

We complete most jewelry appraisals remotely through our online platform, where clients submit high-resolution photographs and any available documentation such as prior appraisals, gemological certificates, or purchase records. Onsite inspection can be arranged for large collections or items requiring hands-on gemological examination. Whether you need a single ring appraised or an entire jewelry estate prepared for donation, our charitable donation appraisals are built to satisfy IRS documentation requirements and withstand audit scrutiny. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Types of Jewelry We Appraise for Charitable Giving

AppraiseItNow appraises a wide range of jewelry items commonly donated to museums, universities, auction-based charities, and nonprofit organizations.

- Diamond engagement rings and wedding sets, including solitaires and multi-stone designs

- Signed designer jewelry from houses such as Cartier, Tiffany, Van Cleef and Arpels, and Bulgari

- Antique and period jewelry including Victorian, Art Nouveau, Art Deco, and Retro pieces

- Loose gemstones including diamonds, rubies, sapphires, emeralds, and colored stones with or without grading reports

- Strand and baroque pearl necklaces, bracelets, and earrings

- Platinum, gold, and silver fine jewelry without significant gemstone content

- Estate jewelry collections donated as a grouped lot to a single donee

- Brooches, pins, and decorative jewelry with historical or collectible significance

- Ethnic and regional jewelry including Native American, Asian, and Middle Eastern pieces

- Costume jewelry with documented provenance or designer attribution that may carry collectible value

How Our Jewelry Donation Appraisal Process Works

- Clients submit photographs and supporting documentation through our secure online platform. For items requiring closer examination, such as stones without grading certificates or pieces with condition concerns, we coordinate an in-person inspection with a credentialed appraiser.

- Our appraisers hold credentials through recognized professional organizations including ISA, ASA, AAA, and CAGA, and bring gemological training to each evaluation. They assess cut, color, clarity, carat weight, metal content, maker's marks, condition, and current secondary market comparables to arrive at a supportable fair market value.

- Each completed appraisal report includes a detailed item description, the valuation methodology, market data supporting the conclusion, the appraiser's credentials, and the signature required for IRS Form 8283 Section B. Reports are formatted to meet IRS qualified appraisal standards under IRC §170(f)(11).

- Appraisals are timed to comply with the IRS window: completed after the 60-day lookback period and before the tax return filing deadline, including any extensions. Clients donating multiple pieces to different organizations receive guidance on how aggregation rules and separate Form 8283 filings may apply to their situation.

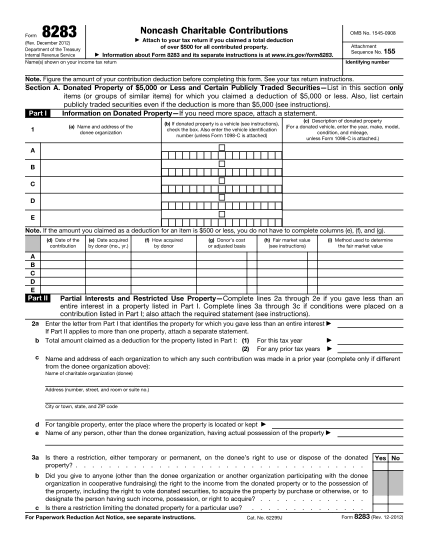

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does a Jewelry appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does a jewelry appraisal for charitable donation involve?

A charitable donation jewelry appraisal is a written, USPAP-compliant report that establishes the fair market value of your jewelry as of the donation date, prepared to meet IRS requirements under Code §170(f)(11)(E) and §6695A. The report documents item descriptions, condition, methodology, comparable market data, and the appraiser's qualifications and signature. It is specifically structured to support a noncash charitable contribution deduction and differs from insurance or replacement value appraisals.

When is a qualified appraisal required for a jewelry donation?

A qualified appraisal is required when the total deduction claimed for donated jewelry exceeds $5,000, including situations where similar items donated to different charities are aggregated to reach that threshold. Donations between $500 and $5,000 require IRS Form 8283 Section A but do not require a formal appraisal. Once you cross the $5,000 mark, Form 8283 Section B must be completed and signed by a qualified appraiser.

What credentials should the appraiser have?

The appraiser must meet the IRS definition of a "qualified appraiser" under Code §170(f)(11)(E), meaning they must have verifiable expertise in jewelry valuation, operate independently from the transaction, and be subject to penalties for substantial overvaluation. AppraiseItNow appraisers hold credentials through recognized professional organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB. They have no financial interest in the donated property and are qualified to sign Form 8283 Section B.

How is jewelry valued for charitable donation purposes?

Jewelry donated to charity is valued at fair market value, which is the price a willing buyer and willing seller would agree upon in an open market as of the donation date. Appraisers use comparable sales data, current market conditions, and a thorough assessment of each piece's condition, materials, and characteristics. Sentimental value and retail replacement cost are not relevant to this standard, as outlined in IRS Publication 561.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are fully USPAP-compliant and prepared to IRS qualified appraisal standards, including proper valuation date documentation, methodology disclosure, appraiser credentials, and a non-contingent fee declaration. This means the appraisal fee is never tied to the value conclusion, which is a core IRS requirement for charitable donation appraisals.

How long does a jewelry appraisal for charitable donation take?

Most remote jewelry appraisals are completed within 7 to 10 days. Onsite inspections or larger collections typically take 2 to 3 weeks. If you have a filing deadline approaching, rush service is available for same-day or next-day turnaround.

What does a charitable donation jewelry appraisal cost?

Advanced jewelry appraisals prepared for IRS-qualified purposes such as charitable donations start at $295 per item, with most projects falling in the $395 to $2,200 range depending on scope. Volume pricing applies to collections, with single-item appraisals typically ranging from $195 to $495, small collections of around 10 items ranging from $695 to $1,200, and larger collections of 50 to 100 or more items ranging from $1,600 to $3,500 or more. Fees are quoted as a fixed price before work begins, based on factors like item count, complexity, and documentation quality. Visit our personal property appraisal page for more detail.

Can you appraise jewelry anywhere in the US?

Yes, AppraiseItNow provides jewelry appraisals nationwide. Remote appraisals are conducted using photographs and documentation you submit, and onsite inspections can be arranged across the country for larger collections or situations that require in-person examination.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow appraisals are prepared to meet qualified appraisal standards, including proper valuation date, documented methodology, appraiser credentials, and a non-contingent fee structure, all of which are key IRS requirements for charitable donation deductions over $5,000. While no appraiser can guarantee acceptance in every context, following these standards significantly reduces the risk of deduction disallowance or audit challenges. If your appraisal is also needed for insurance or legal purposes, let us know so the report can be scoped appropriately.

When exactly does the appraisal need to be completed relative to my donation date?

The appraisal cannot be dated more than 60 days before the date the charity accepts and receipts your jewelry donation. It must also be completed no later than your tax filing deadline, including any extensions you file. Keeping the appraisal within this window ensures the fair market value reflects conditions at the time of the actual donation.

If I donate jewelry to multiple charities, does the combined value trigger the appraisal requirement?

Yes, if the pieces are considered similar items under IRS rules, their values are aggregated across all recipients to determine whether the $5,000 threshold is met. A single appraisal report can cover multiple pieces grouped by category, even if they are going to different charitable organizations. Items that are not similar in nature are evaluated separately and do not aggregate toward the threshold.

Do multiple rings or similar jewelry pieces count together toward the $5,000 IRS threshold?

Yes, the IRS requires similar items to be aggregated when calculating whether your total deduction exceeds $5,000, even if individual pieces are worth less than that amount on their own. This aggregation rule applies regardless of whether the items are donated to the same charity or to different organizations. If the combined value of similar pieces exceeds $5,000, a qualified appraisal and Form 8283 Section B are required.

What IRS form is required for a jewelry donation appraisal over $5,000?

IRS Form 8283 Section B is required for noncash charitable contributions exceeding $5,000, and it must be signed by the qualified appraiser before you file your return. If the total value of donated jewelry or collectibles exceeds $20,000, a copy of the appraisal itself must also be attached to your tax return. Section A is used for donations between $500 and $5,000 and does not require an appraisal.

What exactly does fair market value mean when appraising jewelry for a charitable donation?

Fair market value is the price at which a piece of jewelry would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell, and both having reasonable knowledge of the relevant facts. For jewelry, this is determined using comparable sales data and current market conditions as of the donation date, not what you paid for the piece or what it would cost to replace it. IRS Publication 561 provides the governing guidance for this standard as it applies to personal property and collectibles.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.