IRS-qualified appraisals for donated sports memorabilia, meeting Form 8283 Section B requirements for deductions over $5,000. AppraiseItNow provides defensible fair market value reports covering autographed items, game-used gear, and trading card collections to protect your deduction.

Best in class appraisers across asset types

.avif)

Joe Kattan

Aron Blue

Sports Memorabilia Appraisals for Charitable Donation

When you donate sports memorabilia to a qualifying nonprofit, the IRS requires a qualified appraisal to substantiate your deduction if the claimed fair market value exceeds $5,000 for an item or group of similar items. That appraisal must be completed no earlier than 60 days before the donation date, and both the appraiser and the donee organization must sign Form 8283 Section B before you file. For collections valued above $20,000, the full appraisal must be attached to your return. Our personal property appraisal services cover the full range of sports collectibles that commonly trigger these requirements.

AppraiseItNow delivers appraisals both online and onsite across the United States, making it straightforward to meet IRS deadlines regardless of where your collection is located. Our appraisers are credentialed through ISA, ASA, AAA, CAGA, AMEA, and NEBB, and specialize in the sports collectibles market. Learn more about our IRS-compliant donation valuation services and how we support donors through the documentation process. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Sports Memorabilia We Appraise for Charitable Giving

AppraiseItNow appraises a wide range of sports collectibles donated to qualifying organizations, including:

- Autographed jerseys, helmets, and uniforms from professional and collegiate athletes

- Game-used equipment such as bats, gloves, balls, and sticks with documented provenance

- Signed photographs, lithographs, and framed displays

- Vintage and modern trading card collections, including graded and raw cards

- Championship rings, trophies, and awards

- Bobbleheads, figurines, and limited-edition memorabilia sets

- Programs, ticket stubs, and scorecards from historically significant events

- Signed books, magazines, and media guides

- Display cases and shadow boxes containing authenticated multi-item collections

- Memorabilia tied to specific games, seasons, or record-breaking moments

How Our Sports Memorabilia Appraisal Process Works

- Appraisers evaluate each item based on condition, provenance, authenticity documentation, and recent comparable sales data from auction records and the broader sports collectibles market. Items with third-party authentication certificates or grading reports are incorporated into the analysis.

- When a donation involves multiple similar items, such as a set of autographed cards or a group of signed jerseys, a single qualified appraisal can cover the entire group. Our reports clearly identify each item, describe the valuation methodology, and meet all IRS content requirements for Form 8283 Section B.

- Completed appraisal reports include the appraiser's credentials, a detailed item description, the effective date of value, the basis for the fair market value conclusion, and the appraiser's signature. Reports are formatted to satisfy Treasury Regulation requirements and withstand IRS scrutiny.

- Appraisals are available online using photographs and documentation you provide, or onsite for large or high-value collections where physical inspection is warranted. Turnaround times are designed to accommodate tax filing deadlines and donation timing requirements.

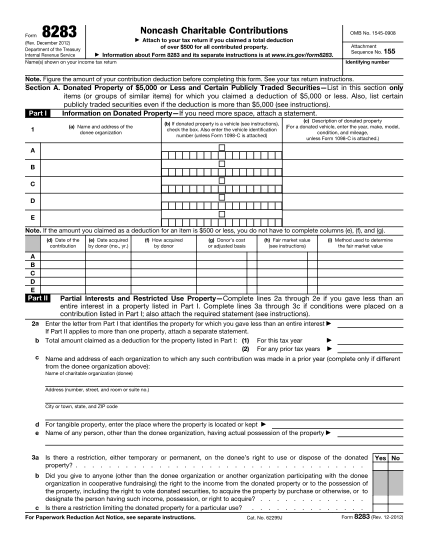

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does a Sports Memorabilia appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does a Sports Memorabilia appraisal for charitable donation include?

A charitable donation appraisal for sports memorabilia determines the fair market value of items such as autographed jerseys, trading cards, or game-used equipment, and is prepared to meet IRS qualified appraisal requirements. The report includes detailed item descriptions, condition assessments, provenance documentation, authenticity review, comparable sales analysis, and the appraiser's credentials. This documentation supports IRS Form 8283 and helps protect your deduction from denial during an audit.

When do you need a qualified appraisal for donated sports memorabilia?

A qualified appraisal is required when the claimed fair market value of a donated item or group of similar items exceeds $5,000, which triggers Form 8283 Section B and requires both appraiser and donee signatures. The IRS aggregates similar items donated to multiple charities within the same tax year, so a $3,000 donation to one organization and a $3,000 donation to another could still cross the threshold. Sports memorabilia faces heightened IRS scrutiny as collectibles, making proper documentation especially important.

What credentials should the appraiser have?

The appraiser must meet IRS "qualified appraiser" standards, including independence from both the donor and the charity, demonstrated experience appraising sports collectibles specifically, and no contingency-based fee arrangements. Credentials from recognized professional organizations such as ISA, ASA, or AAA, combined with documented education and training in the relevant category, are key indicators of qualification. General appraisers without sports memorabilia expertise risk IRS rejection of the report.

How is fair market value determined for sports memorabilia donated to charity?

Appraisers determine fair market value by analyzing what a willing buyer would pay a willing seller in an open market, drawing on condition, rarity, provenance, authenticity documentation, and recent comparable sales for similar items. Factors such as event associations, prior ownership history, and the availability of certificates of authenticity all influence the final value conclusion. This FMV figure is what gets reported on Form 8283 to substantiate your deduction.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are prepared in compliance with the Uniform Standards of Professional Appraisal Practice (USPAP). Our appraisers are credentialed through recognized professional organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB, and reports prepared for charitable donation purposes meet IRS qualified appraisal requirements.

How long does a Sports Memorabilia appraisal take?

Most remote appraisals are completed in 7 to 10 days, while onsite inspections or larger collections typically take 2 to 3 weeks. If you have a filing deadline or time-sensitive donation, rush service is available for same-day or next-day turnaround.

What does a charitable donation appraisal for sports memorabilia cost?

Advanced appraisals prepared for charitable donation purposes start at $295, as they require an IRS-qualified report with additional compliance elements beyond a standard appraisal. Typical project fees range from $395 to $2,200, with single-item appraisals generally running $195 to $2,000 and small collections of around 10 items ranging from $695 to $3,000. Larger collections of 50 to 100 or more items are priced at $1,600 to $5,000 or more, with volume discounts applied. Fees are quoted as a fixed price before work begins, based on factors such as the number of items, complexity, provenance quality, and intended use. Visit our personal property appraisal page for more detail.

Can you appraise Sports Memorabilia anywhere in the US?

Yes, AppraiseItNow provides sports memorabilia appraisals nationwide. Remote appraisals are available for clients across all 50 states, and onsite inspections can be arranged for larger or more complex collections.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow appraisals for charitable donation are prepared to meet all qualified appraisal requirements, including a proper valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration. While no appraiser can guarantee acceptance in every circumstance, following these standards significantly reduces the risk of denial or challenge. Reports are structured to support Form 8283 and withstand IRS scrutiny, which is especially important given the heightened attention collectibles like sports memorabilia receive.

Do trading cards need a separate appraisal from other sports collectibles?

Trading cards are treated as similar items by the IRS, meaning their total fair market value is aggregated across donations to different charities within the same tax year, and a single qualified appraisal can cover the group if they cross the $5,000 threshold together. However, dissimilar item types, such as trading cards and autographed jerseys, are evaluated separately, and each category exceeding $5,000 requires its own appraisal and Form 8283 Section B filing. A single report can cover multiple dissimilar items donated to the same charity on the same date.

How does provenance affect the value of donated sports memorabilia?

Strong provenance, including documented ownership history, event associations, prior sale records, or media verification, can meaningfully increase the fair market value of sports memorabilia by reinforcing authenticity and buyer confidence. Appraisers are required to address provenance in the report, as it directly influences the comparable sales analysis and the final value conclusion reported on Form 8283. Weak or missing provenance can lower the appraised value and raise questions during an IRS audit.

When does the appraisal need to be completed relative to the donation date?

The appraisal must be signed and dated no earlier than 60 days before the donation is made, and it can be completed any time up to the due date of the tax return on which you claim the deduction, including extensions. Preparing the appraisal too early risks invalidating it for IRS purposes, so timing matters. Retain the completed appraisal with your records in case of an audit.

What happens if you skip the appraisal for a group of signed sports photos worth more than $5,000?

Without a qualified appraisal, the IRS will deny the charitable deduction for similar items exceeding $5,000 in total fair market value, regardless of how well-documented the donation itself is. Courts have upheld this denial in cases where donors failed to obtain a compliant appraisal, and the IRS may also assess penalties for gross valuation misstatements. The aggregation rule applies even when donations are split across multiple charities, so the threshold can be reached more easily than donors expect.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.